Investor home bias

The lifting of exchange controls and the globalisation of financial markets has opened the door to international diversification and its benefits. However, many investors still overweight their home markets, more so at times of relative outperformance. It would be better to avoid ‘putting all your eggs in one basket’. Miguel de Cervantes first advised this in his 1615 novel Don Quixote, where he wrote: “It is the part of a wise man to keep himself today for tomorrow, and not to venture all his eggs in one basket.”

Home bias is a recurring focus in international portfolio theory. By 1991, Kenneth French and James Poterba had already referred to this in their paper on investor diversification and international equity markets.1

Home bias can be the result of what in economic theory is known as information asymmetry. The lack of information on other opportunities such as investments in other countries, in other securities’ markets or foreign currencies can be reasons for home bias. It can also be the result of regulation, when there are limits on foreign currency denominated assets, credit rating limitations for bonds, or single name limitations. This primarily applies to institutional investors. The Organization for Economic Cooperation and Development (OECD) does regular updates and surveys on these restrictions.[1] In addition, large pension funds and insurance companies can impose additional limitations on currency exposures or domestic bond portfolios for liability matching.

Private wealth is not burdened by the same restrictions. It is a common assumption that home bias had reduced significantly since 1980. According to an Ernst & Young study, the home bias of US investors had declined by 20% since 1980.[2] The opening of emerging markets and development of capital markets in Europe have both contributed positively to this trend. Another example was a Vanguard study from 2017 which showed that 40% of clients and advisors ranked geographic diversification as a Top 3 need.[3]

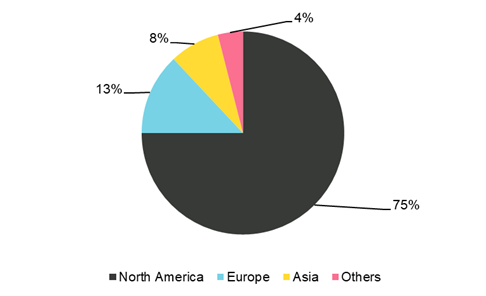

However, this trend seems to have reversed in the last decade. According to a survey by the International Monetary Fund (IMF), US investors put approximately 80% of their wealth into US denominated assets – even though the US capital market only accounts for around 50% of total world market capitalisation, and the US economy contributes only a quarter to worldwide GDP in nominal terms and around 16% in real terms.

This investment strategy disregarded many investment opportunities outside the US in periods when foreign assets outperformed US assets. During the period from early 2004 to the end of 2011, which included the Great Recession and the start of the banking crisis in the European Union, European and Asian equities outperformed US equities by a factor of seven.

Home bias of US investors

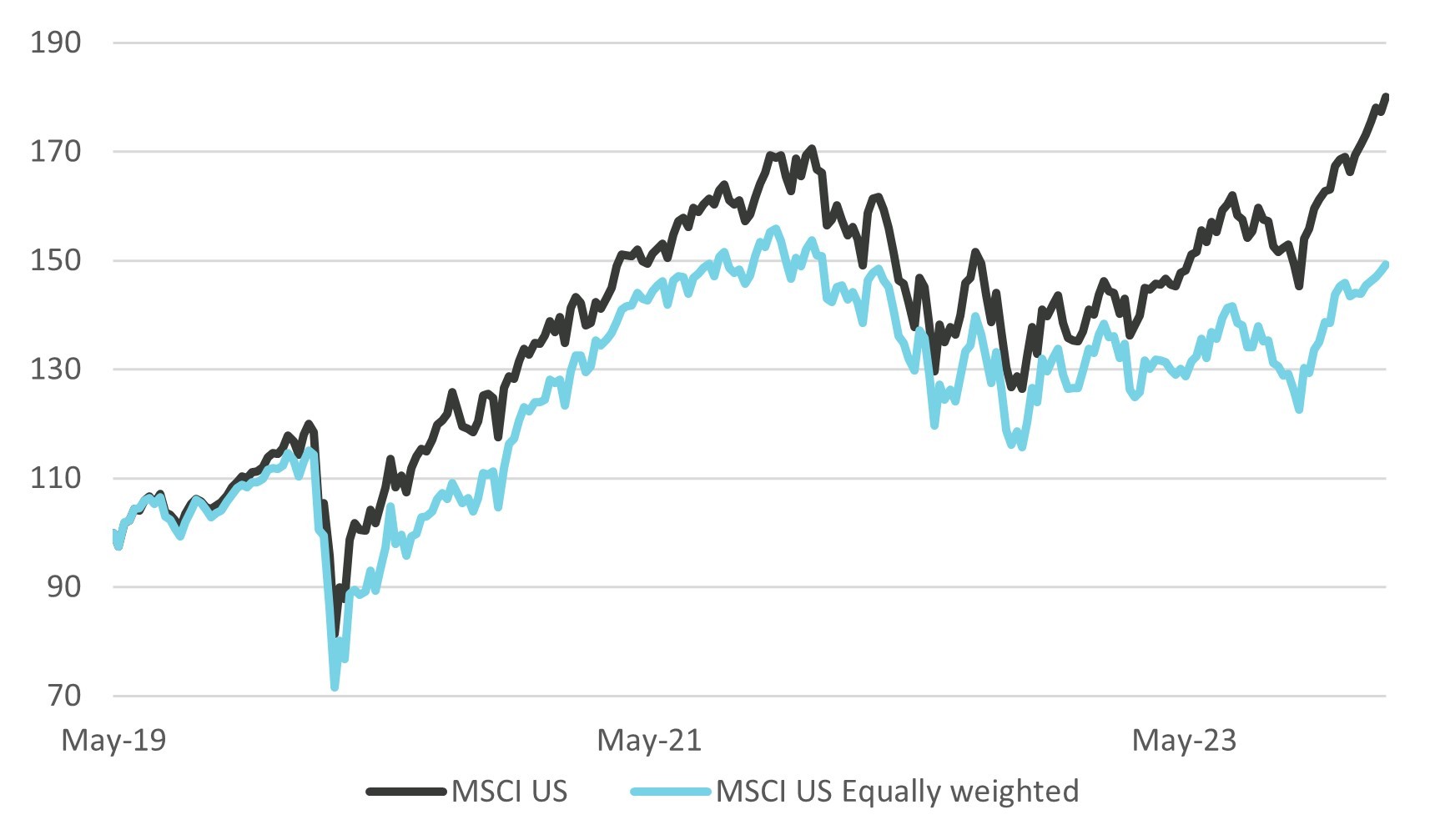

Diversification can also be compromised by the sector concentration and composition of the equity index. US technology is a relatively large sector and the mega tech companies known as the Magnificent 7 have driven the US equity market higher. The graph below shows that the Morgan Stanley Capital International (MSCI) index in the United States is disproportionately driven by a few large companies. The gap between the MSCI USA index based on market capitalisation (the black line) and the index based on equal weights (the blue line) has been growing.

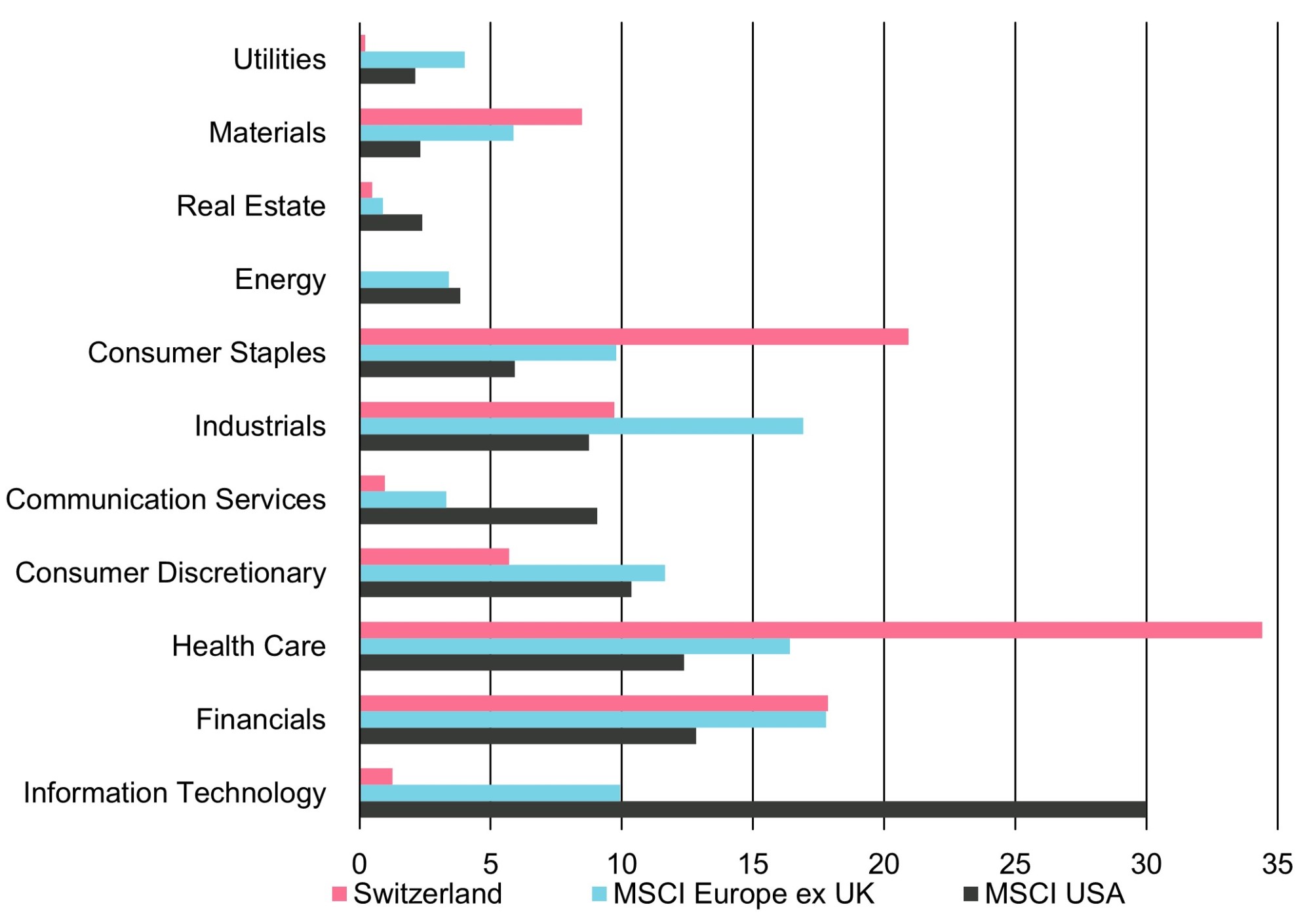

A second factor is that, as noted above, the MSCI USA, like the S&P 500, is less diversified in terms of sectors than its European equivalent. This is shown in the graph below. The continued outperformance of the US technology sector has increased its market capitalisation and its weighting in portfolios. This translates to higher US home bias and further concentration of risk in portfolios.

A European equity investor with a higher allocation to European equities will achieve more international diversification than a US equity investor with a similar home bias. This is because the European equity universe is more diverse, and equity benchmarks are more globally exposed. According to Goldman Sachs the Eurostoxx 600 index has 60% of revenues stemming from outside of the Euro area compared to 30% for the S&P 500, 40% for the Japanese Topix, and 25% for the MSCI Emerging Markets index.

We conclude that while the US investor’s home bias has recently benefited from the strong performance of a higher tech allocation and the Magnificent 7, US investors have enjoyed less benefits from diversification. The dominance of the Magnificent 7 has clearly given rise to more concentration risk. International diversification would provide US investors with exposure to other return drivers, and lower concentration risk and volatility.

1 French, K. R. and Poterba, J. M. (1991). Investor diversification and international equity markets. American Economic Review Papers and Proceedings, 81, 222–226.

[1] OECD. (2021). Annual survey of investment regulation of pension funds and other pension providers. https://www.oecd.org/daf/fin/private-pensions/2021-Survey-Investment-Regulation-Pension-Funds-and-Other-Pension-Providers.pdf

[2] Ernst & Young. (2014). Wealth management study.

[3] Vanguard. (2017). The global case for strategic asset allocation and an examination of home bias.

[4] In Asia, the home bias of more than 80% is even more pronounced than in the US.

/https://storage.googleapis.com/ggi-backend-prod/public/media/5345/Laptop---smartphone-square.jpg)

/https://storage.googleapis.com/ggi-backend-prod/public/media/5347/caron_nicolas_890x500px-bw-sq.jpg)

/https://storage.googleapis.com/ggi-backend-prod/public/media/5348/Vontobel-Swiss-Financial-Advisers_NEW-Dec-2023.png)

/https://storage.googleapis.com/ggi-backend-prod/public/media/7304/0618824f-f10f-4e30-90c2-02952092b9db.jpg)

/https://storage.googleapis.com/ggi-backend-prod/public/media/7367/12cc585b-6096-4511-928c-efa3eccb364b.jpg)

/https://storage.googleapis.com/ggi-backend-prod/public/media/3193/coffee-farm-a148234519.jpg)